Earn cash back

after close!

With Home Connect, you could earn $350 to $9,500 cash back after close.

You saved for ages (or at least what seemed like it) before buying your home, and you invested even more time and money during your years of ownership. But what if something happens to your home and everything you worked so hard for? Could you afford to rebuild and replace it all? For most people, the answer, tragically, is “no.”

Thankfully, having the right homeowners insurance coverage can safeguard your home and other valuable items. Purchasing an insurance policy can protect against damage to your home, damage to your personal possessions, and your assets from any liability claims — from fires to personal injuries, theft or even pet-related incidents.

In the United States, the average home insurance premium costs $1,192 a year. Additionally, the median home value is $257,445 nationwide.

Here’s what you need to know to ensure you’re protected against the unexpected.

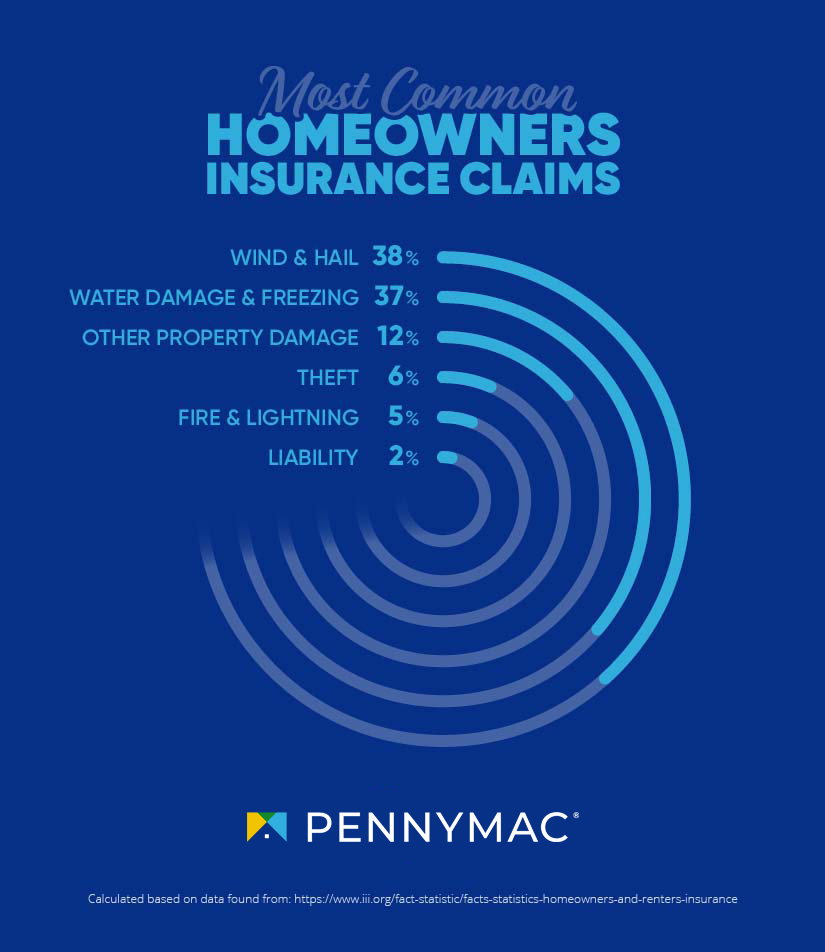

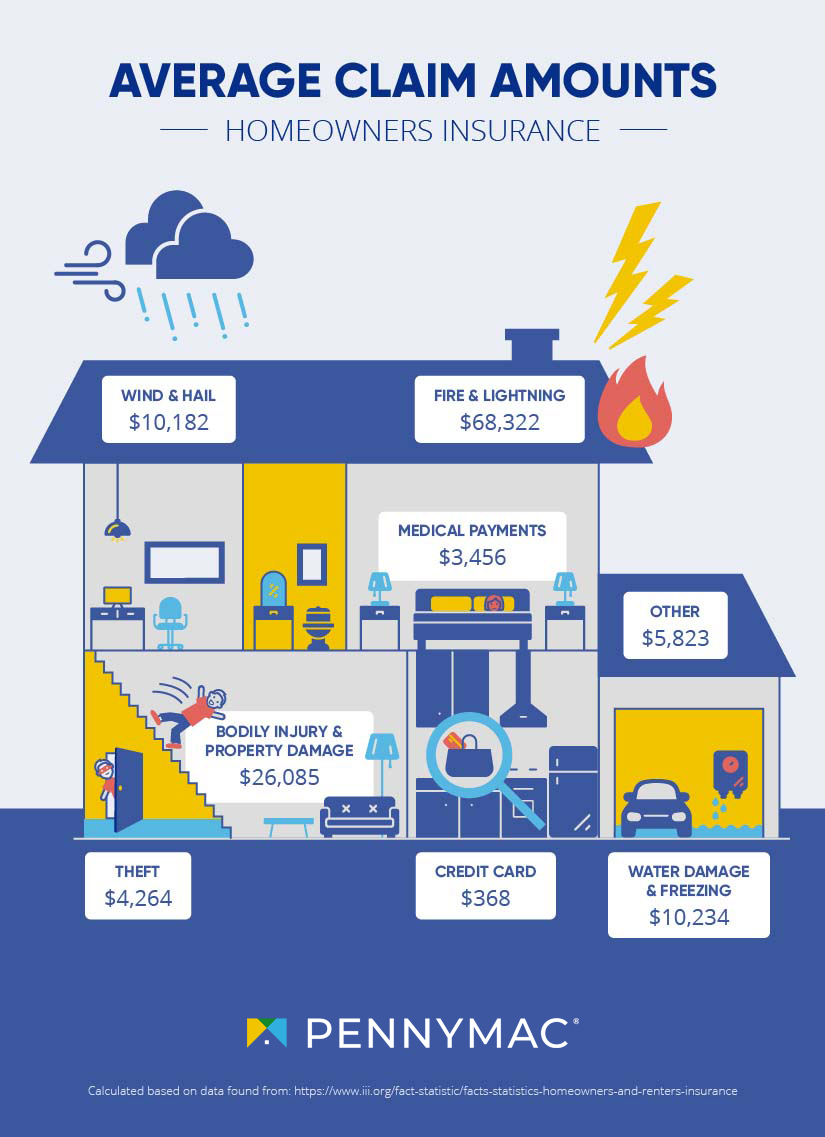

What Does Homeowners Insurance Cover?

Common perils covered by most homeowners insurance policies can include the following:

- Fire and smoke damage

- Hail damage

- Lightning strikes

- Windstorms, such as tornadoes

- Theft or vandalism

- Water damage from plumbing leaks

- Explosions from gas lines

- Damage from vehicles or aircraft

There are many different types of policies available, ranging from basic to comprehensive. You will need to work with your insurance agent to determine the right coverage for your home. When you shop for your homeowners policy, you will need to consider multiple factors, including the features of your home, the region you live in, and what coverage is available to you.

About 60 percent of all U.S. homes are underinsured by an average of 20% according to CoreLogic, a company based in Irvine, Calif., that provides data to most major home insurers.

What is Covered by a Standard Policy

When protecting your home from the risks listed above, your homeowners insurance will provide coverage in five major ways: dwelling coverage, coverage for other structures, personal property coverage, liability protection, and loss-of-use coverage. Here’s how each part works to help you.

Dwelling vs. Personal Property Coverage

Confused by where dwelling coverage ends and personal property coverage starts? If you could pick your home up and shake it, anything that would fall out is insured by personal property coverage. For example, your kitchen cabinets would be covered by dwelling coverage, but your furniture would fall under personal property coverage.

Loss of Use Coverage

If you experience significant damage to your home, it is likely that your home may be uninhabitable during the repair process. If you need to temporarily move out of your home, loss-of-use coverage will pay for additional housing and living expenses, such as a hotel or rental.

Looks like you’re on your way to understanding all the responsibilities that come with homeownership. To find out if you’re ready to take the next step, check out Is Homeownership Right for You?

What Isn’t Covered by Homeowners Insurance

You may think that your policy has the features that you need, but are you sure that you have checked it carefully? On many homeowners insurance policies, there are potentially devastating disasters and damages that are not covered.

For example, damages caused by “Acts of God” are typically not covered. Defined as events outside of human control or activity, the most common “Acts of God” include earthquakes, tornadoes, and floods. The most common of these is flood insurance, which can be purchased in addition to homeowner’s insurance, and is required by most lenders if you live in a high risk flood zone. If you live in an area where these types of natural disasters are common, it is worthwhile to purchase separate insurance policies to protect your home and personal property against these risks.

More than half of all homeowners, 56%, falsely believe that flood damage is covered by their standard policy, according to the survey by insuranceQuotes in partnership with Princeton Survey Research Associates International.

Another common exclusion is “Acts of War,” which means that losses from events such as invasions, insurrections, riots, strikes, revolutions, military coups and terrorism would not be covered. Separate war risk protection can be obtained to cover damage from these events.

Is Homeowners Insurance Legally Required?

It may surprise you to learn that most states don't legally require you to have homeowners insurance. However, mortgage lenders do require it. When you first request a mortgage on the home you want to buy, you will need to provide proof of homeowners insurance on the property before the lender will move forward with your loan.

This is because the lender is your partner when you buy a home with a mortgage, and they want to make sure that their investment is protected. Shop around and choose the best coverage for yourself.

Homeowners insurance is one of several important steps in securing a mortgage. For an in-depth look at the entire process, check out our six-part series Explaining the Home Loan Process.

Peril Protection is Only a Policy Away

Hopefully, as a homeowner, you will not have to deal with the major damage brought on by a fire or plumbing issue, and it's unlikely that you will never experience any damage to your home or possessions in your lifetime. However, knowing you have the homeowners insurance coverage you need makes the difference when these unexpected pitfalls occur.

Below are some tips on keeping your premiums low:

- Get a new quote every year from various companies.

- Install an outdoor light and motion-activated camera.

- Equip your home with a fire extinguisher and carbon monoxide detector.

- Buy a home security system.

It is also a good idea to check with your insurance provider, they may have additional ways to keep costs low.

Ready to find the right partner who can help you make the smartest purchase on your home? Contact a Pennymac Loan Officer today.

Share

Categories